The Inverted Duty Structure (IDS) under the Goods and Services Tax (GST) regime is a situation where the rate of tax on inputs (raw materials or services) is higher than the rate of tax on output supplies (finished goods or services). This creates an imbalance, as businesses end up paying more GST on inputs than they can offset against the GST on their outputs, leading to an accumulation of Input Tax Credit (ITC).

To address this issue, the GST law provides a mechanism for refunds of unutilized ITC in cases of an inverted duty structure. Below is a detailed explanation of the concept, its implications, and the refund mechanism under GST:

According to section 54(3) refund of unutilised credit can be availed where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies), except supplies of goods or services or both i.e., in case of inverted duty structure.

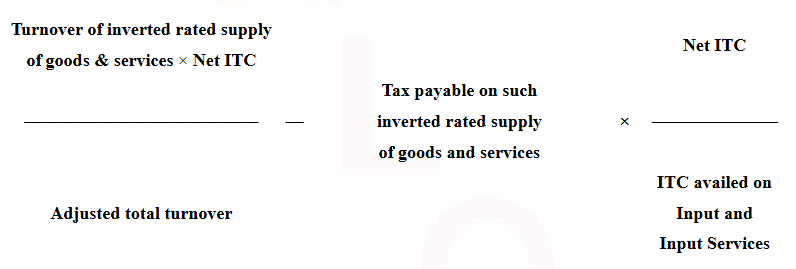

Calculation of Maximum Amount of refund under Inverted Duty Structure [Rule 89(5)]:

Rule 89(5) stipulates that in the case of refund on account of inverted duty structure, maximum refund of ITC shall be granted as per the following formula:

Let’s discuss various elements of this formula:

Where:

- Net ITC: Input tax credit availed on inputs and input services during the relevant period.

- Turnover of Inverted Rated Supply: The value of supplies with a lower GST rate (output supplies).

- Adjusted Total Turnover: Total turnover of the business during the relevant period.

- Tax Payable on Inverted Rated Supply: Output tax liability on inverted rated supplies.

1. Net ITC:Net ITC means ITC availed on inputs during the relevant period other than the ITC availed for which refund is claimed under sub-rules (4A) or (4B) or both. Now it is noteworthy that in the meaning of net ITC only Inputs is covered and not Capital goods or services. So, it is quite clear that law and related rules prevent the refund of tax paid on input services and Capital goods as part of refund of ITC accumulated on account of inverted duty structure.

If there are more than one input, with different rates of GST, ITC availed on all inputs shall be included ‘Net ITC’. For example, if input A (attracting 5% GST) and input B (attracting 18% GST) to manufacture output Y (attracting 12% GST), and ITC availed on A is Rs.500 and on B is Rs.360 then net ITC, irrespective of their rate of tax, shall be Rs.860.

2. Adjusted Total Turnoveris calculated by adding:

(a) The turnover in a State or Union territory, excluding the turnover of services, as defined under section 2(112).

(b) The turnover of Zero-rated supply of services, which means the value of Zero-rated supply of services made without payment of tax under bond or LUT, calculated in the following manner:

Zero-rated supply of services is calculated by adding up payments received during the relevant period for such services. This value also includes completed services where payment was received in advance before the relevant period. However, it subtracts advances received for services that haven`t been completed during the relevant period.

Exclusions from the calculation of Adjusted Total Turnover include:

(i) The value of exempt supplies other than zero-rated supplies.

(ii) The turnover of supplies in respect of which refund is claimed under sub-rule (4A) or sub-rule (4B) or both, if any, during the relevant period

3. Relevant period: Relevant period means the period for which the claim has been filed.

Now let us understand the whole calculation of maximum refund with the help of an example:

Certainly, let`s consider a manufacturing scenario where a company produces goods, namely Product X, which falls under the 12% GST rate category. The manufacturing process involves the use of raw materials – raw material A (5% GST) and raw material B (18% GST). For simplicity, let`s exclude any input services.

Assuming the company exclusively produces and sells Product X during the relevant period, the adjusted total turnover equals the total sales value of Product X. Suppose the company sells Product X with a value of 3,000/-.

In the same period, the company procures raw material A and B with respective values of 1000/- and 2000/- for manufacturing Product X. The Net ITC is calculated as 500/- (50/- for raw material A and 410/- for raw material B).

Applying the formula from rule 89(5), the maximum refund amount can be computed as

resulting in a maximum refund amount of Rs.50.

Let us take another example to understand the calculation of Maximum Refund Amount under Rule 89(5):

Suppose ABC ltd., a registered supplier in Chhattisgarh, is engaged in supply of taxable goods within the State. Given below are the details of the turnover and applicable GST rates of the final products manufactured by ABC ltd. as also the Input tax credit (ITC) availed on inputs used in manufacture of each of the final products and GST rates applicable on the same, during a Tax period:

| Products | Turnover | Output GST Rates | ITC availed | Input GST Rates |

| P | 500000 | 5% | 54000 (Goods) | 18% |

| Q | 350000 | 5% | 54000 (Goods) | 18% |

| R | 100000 | 18% | 10000 (Services) | 18% |

It has also been provided that Product Q is notified as a product, in respect of which no refund of unutilised Input tax credit shall be allowed under said section.

The maximum refund amount which ABC ltd is eligible to claim shall be computed as follows:

Tax payable on inverted rated supply of Product P = 5,00,000 × 5% = 25,000

Net ITC = 108000 (54,000 + 54,000) [Net ITC availed during the relevant period needs to be considered irrespective of whether the ITC pertains to inputs eligible for refund of inverted rated supply of goods or not – Circular No. 79/53/2018-GST dated 31.12.2018]

Adjusted Total Turnover = 9,50,000 (5,00,000 + 3,50,000 + 1,00,000)

Turnover of inverted rated supply of Product P = 5,00,000

Maximum refund amount for ABC ltd is as follows:

= [(5,00,000 × 108000)/ 9,50,000] – (25,000 x 108,000/118,000)

= 33,961

Now another question arises whether inversion created due to change in rate of GST on same goods is eligible for refund under inverted duty structure?

It has been clarified that situations where the GST rate on certain goods changes, leading to an inverted duty structure, the applicant may not be eligible to seek a refund of unutilized Input tax credit (ITC) under this section. For instance, if an applicant initially purchases goods “X” with an 18% GST rate, and later the rate is reduced to 12%, such scenarios are not covered under section 54(3)(ii).

Further another question arises, that when the inversion is created due to lesser rate on output than input due to concessional notification on output?

It has been clarified by Circular No. 135/05/2020-GST dated 31.03.2020 as amended by Circular No. 173/05/2022 GST dated 06.07.2022. In situations where the rate of tax on the output supply is less than the rate of tax on inputs due to a concessional notification, suppliers can be eligible for a refund of accumulated Input tax credit (ITC) under the provisions of clause (ii) of the first proviso to section 54(3). This applies unless the output supply is either Nil rated or fully exempted, and the goods or services supplied are not excluded from the refund of accumulated ITC under the government`s notification. Notably, suppliers who provide goods to merchant exporters at the concessional rate of 0.1% (0.05% CGST and 0.05% SGST/UTGST or 0.1% IGST) under specific notifications are also entitled to a refund on account of an inverted tax structure.

Examples of Inverted Duty Structure (IDS)

- Textile Industry:

- Input GST Rate: 12% (on yarn).

- Output GST Rate: 5% (on fabric).

- Result: Accumulation of ITC due to higher input tax.

- Pharmaceutical Industry:

- Input GST Rate: 12% or 18% (on raw materials).

- Output GST Rate: 5% (on medicines).

- Result: Accumulation of ITC.

- Fertilizer Industry:

- Input GST Rate: 18% (on raw materials).

- Output GST Rate: 5% (on fertilizers).

- Result: Accumulation of ITC.